Market News

Week ahead: Crude oil prices, FIIs activity, US PCE data, Strait of Hormuz among key market triggers to watch

.png)

4 min read | Updated on June 21, 2026, 09:58 IST

SUMMARY

Indian markets enter a shortened trading week with NIFTY50 facing a key hurdle near 24,100 after a two-week recovery. Investors will track crude oil and Strait of Hormuz developments, FII flows, the rupee and US PCE inflation data. A decisive close above 24,100 could extend the recovery towards 24,500, while the 23,700 to 23,800 zone remains the immediate support to watch.

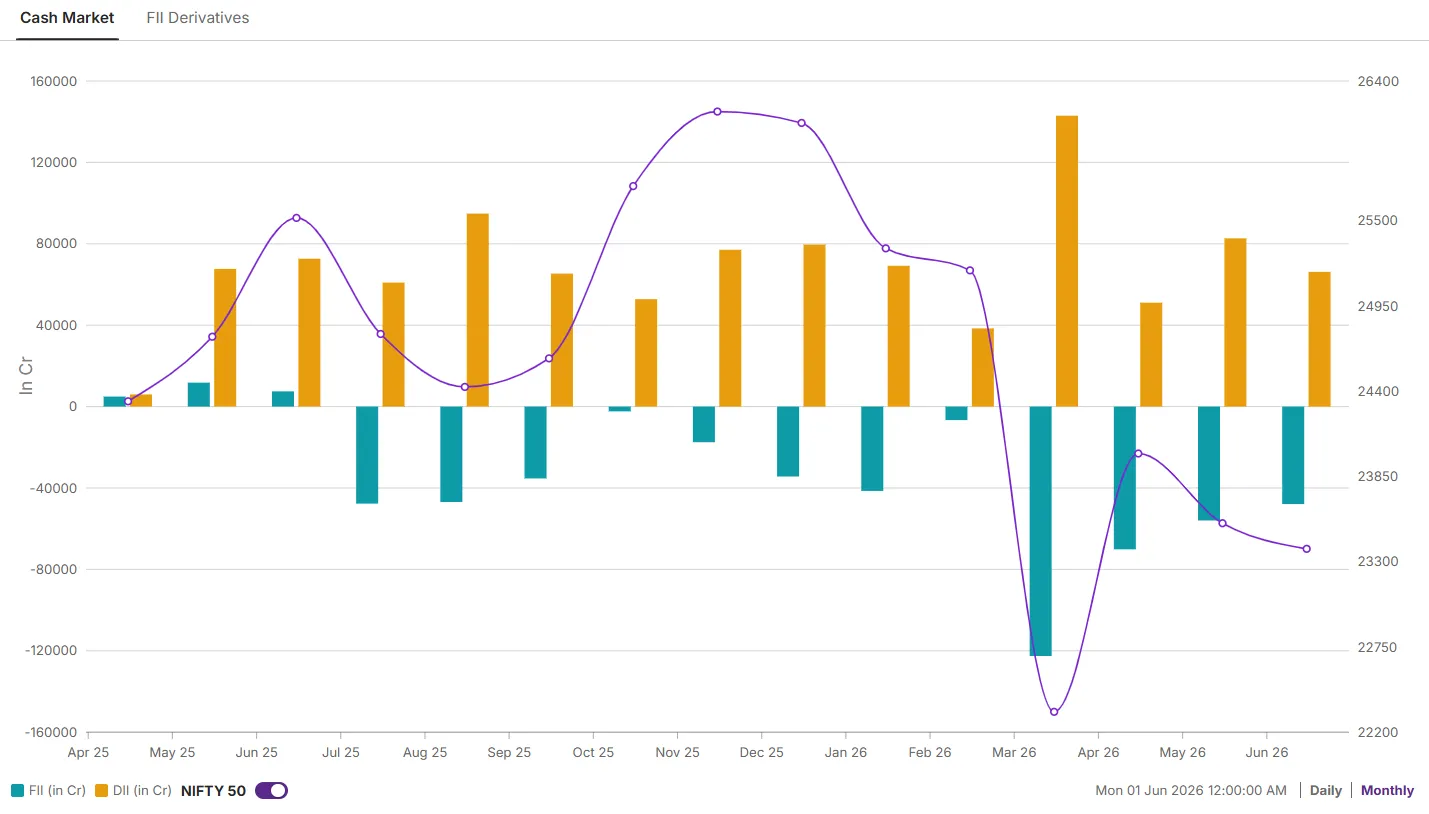

FIIs continued to remain net seller in the cash market, offloading equities worth ₹43,000 crore so far in June.

Indian markets ended higher for the week ended June 19, despite profit booking in the final session after a five-day rally. The NIFTY50 fell 0.6% on Friday to close at 24,013, while the SENSEX declined 0.7% to 76,802. However, both benchmarks still gained around 1.7% for the week, helped by a sharp fall in crude oil prices earlier in the week.

The broader market outperformed the benchmarks, indicating that buying interest remained healthy beyond index heavyweights. Midcap and smallcap stocks continued to attract flows during the week with both Midcap 150 and Small cap 250 indices gaining over 3% respectively. The outperformance remains important to track, as it reflects whether risk appetite remains intact amid volatility in crude oil, the rupee and global markets.

Sectorally, Defence (+6.6%), Consumer Durables (+6.4%), Tourism (+6.0%) and Real Estate (+5.5%) led the rally, reflecting strong risk appetite. IT (-1.3%) was the only sectoral loser, as Accenture’s cautious commentary renewed concerns about the pace of recovery in global technology spending.

Stock-specific action was sharp. Paras Defence surged by 24% over two sessions, and BEL, GRSE, HAL, Mazagon Dock, Bharat Dynamics, Cochin Shipyard and Data Patterns also moved higher.

US earnings will be in focus with FedEx reporting its earnings on Tuesday followed by Micron Technology on Wednesday, with investors closely watching its outlook on memory-chip demand and AI-linked spending.

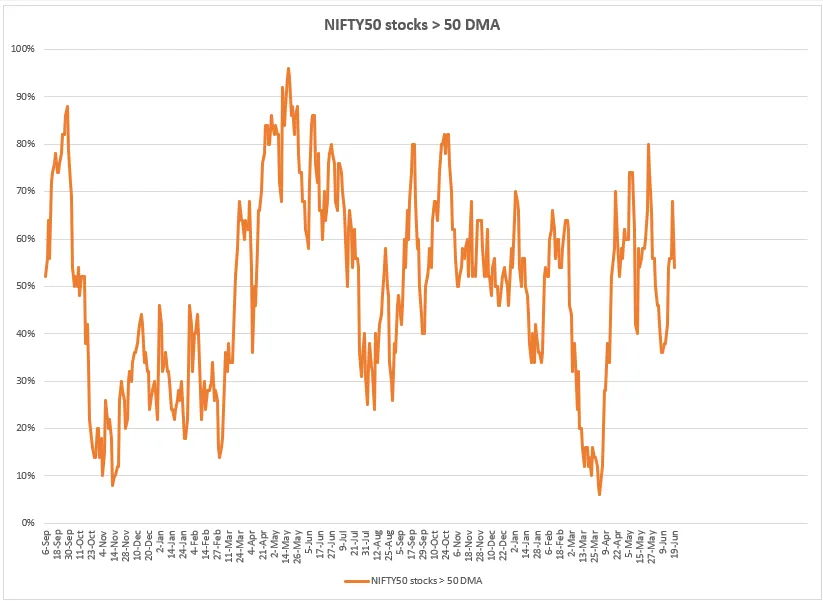

Market breadth

Market breadth improved during the week, supporting the recovery in the broader indices. The share of NIFTY50 stocks trading above their 50-day moving average rose to around 55% by June 19, from nearly 36% at the start of the week.The improvement suggests that buying extended beyond a handful of heavyweight stocks, in line with the outperformance seen in midcaps and smallcaps.

Foreign investors positioning

Foreign investors continued to remain on the selling side in the cash market, offloading equities worth around ₹43,000 crore so far in June. This follows selling of nearly ₹55,963 crore in May, indicating that foreign flows have remained cautious despite the recent recovery in the NIFTY50.

NIFTY50 outlook

NIFTY50 ended the week at 24,013 after facing selling pressure near the 24,200 zone. This area coincides with a falling trendline from the April high, making it the immediate hurdle for the index. The inability to sustain above this level on Friday shows that bulls still need follow-through buying to extend the recovery.

A decisive close above 24,100 would strengthen the near-term setup and open the way towards 24,570, followed by the 200-day EMA near 24,490. On the downside, the 20-day and 50-day EMAs, placed around 23,715 and 23,815 respectively, form the immediate support zone.

Disclaimer:

Derivatives trading must be done only by traders who fully understand the risks associated with them and strictly apply risk mechanisms like stop-losses. We do not recommend any particular stock, securities, or trading strategies. The securities quoted are exemplary and not recommendatory. The stock names mentioned in this article are purely to show how to do analysis.

About The Author

Next Story