Personal Finance News

How to use Public Provident Fund and National Pension System for tax-free income

4 min read | Updated on November 08, 2025, 10:11 IST

SUMMARY

PPF and NPS help you build long-term wealth while offering income tax benefits, but they work differently. The real advantage comes from knowing how to use both together for maximum tax-free income.

Under the new tax regime, you lose the upfront tax deduction benefit on your personal investments in PPF and NPS. | Image: Shutterstock

When it comes to saving for retirement and reducing tax outgo, two of the most reliable tools for Indian investors are the Public Provident Fund (PPF) and the National Pension System (NPS).

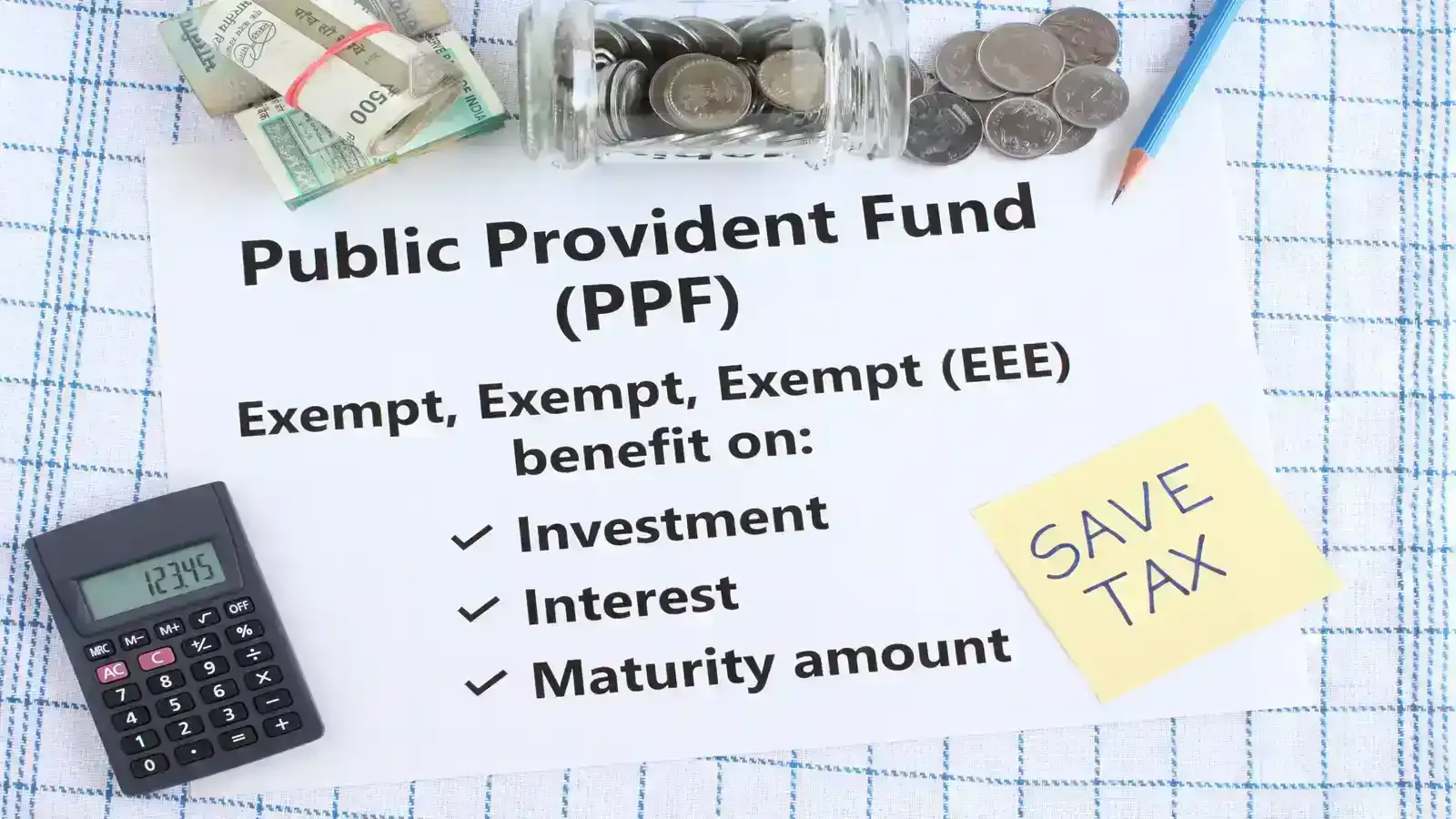

Public Provident Fund (PPF)

What makes PPF stand out is its EEE (Exempt-Exempt-Exempt) status, which means your investment, interest, and maturity proceeds are all exempt from tax.

“Maturity proceeds are also fully exempt under Income Tax laws. The exemption in respect of interest applies during the original 15-year tenure and any extension period. Even if the account isn’t extended but the balance earns interest, that interest too remains tax-free,” explained Balwant Jain, Mumbai-based tax and investment expert.

In the new tax regime, you don’t get a tax deduction on the amount invested, but the interest and maturity proceeds continue to remain completely tax-free.

National Pension System (NPS)

“NPS gives better returns in the long run but also involves some risk since it depends on market performance. It’s ideal for those who want higher growth along with additional tax deductions,” said Abhishek Soni, CEO & Co-founder of Tax2win.

Here’s how NPS benefits work:

-

Deduction up to ₹1.5 lakh under Section 80C.

-

An additional ₹50,000 deduction under Section 80CCD(1B) — exclusive to NPS investors.

-

Under Section 80CCD(2), salaried employees whose employers are enrolled in the NPS can claim this deduction, which is capped at 10% of their basic salary under the old tax regime.

This deduction is applicable in both the new and old tax regimes. This benefit is over and above the Section 80C limits.

-

At retirement (age 60): 60% of the corpus withdrawn is tax-free.

-

40% must be used to buy an annuity, which provides a regular pension.

“Partial withdrawals from the NPS account are exempt up to 25% of the contribution, while the remaining 75% is taxable. On retirement, 60% of the corpus is tax-free, and 40% has to be invested in an annuity that generates taxable pension income,” explained Jain.

However, employer contributions (up to 14% of Basic salary) remain tax-deductible under Section 80CCD(2). Finance Minister Nirmala Sitharaman made this announcement during the presentation of Budget 2024.

Should you choose PPF, NPS, or both?

If you want guaranteed, risk-free, and tax-free returns, go with PPF. If you want higher long-term returns and extra tax benefits, include NPS.

“If you want safe, tax-free, and guaranteed returns, PPF is enough. But if you want to save more tax and earn higher returns, invest in both, PPF for safety and tax-free income, and NPS for long-term growth. Together, they help you balance safety, growth, and tax savings for a secure retirement,” said Abhishek Soni.

So, under the new tax regime, you lose the upfront tax deduction benefit on your personal investments in PPF and NPS. However, the employer’s contribution to NPS and tax-free maturity in PPF continue to offer strong incentives.

Both remain valuable, PPF for its tax-free maturity and NPS for the continuing deduction on employer contributions and long-term growth potential.

Related News

About The Author

Next Story