Personal Finance News

Torn or damaged ₹100, ₹500 notes: RBI rules on exchange, value and where to go

4 min read | Updated on June 13, 2026, 08:04 IST

SUMMARY

RBI rules say torn, soiled and damaged currency notes can still be exchanged. Know how much money you can get back and where to redeem them.

RBI also makes it clear that banks should ensure “none of the bank branches should refuse to accept small denomination notes and/or coins tendered at their counters.”

We all have faced this at some point. You receive a torn ₹100 or slightly damaged ₹500 note and wonder what do about it, if it’s even worth keeping, has it lost it's value. Some try to spend it quickly, others simply discard it.

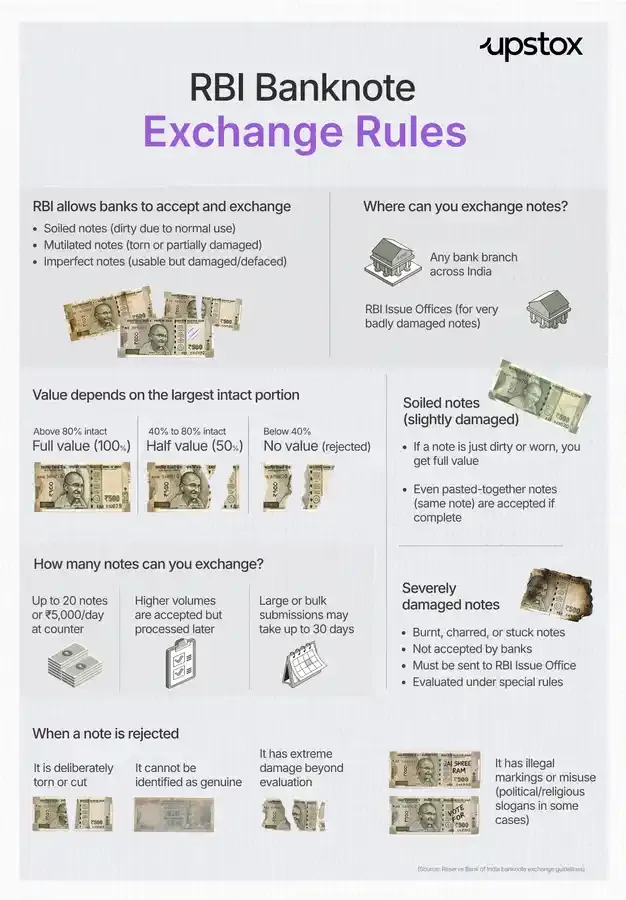

But that’s not how the Reserve Bank of India (RBI) sees it. According to RBI guidelines, “soiled, mutilated and imperfect notes continue to be legal tender.” That means even if your note looks damaged, it is still valid money and in many cases, you can still exchange it for its full value.

In its banknote exchange guidelines, the central bank says banks are “advised to accept soiled/mutilated/ defective notes for exchange at all its branches on all working days.”

So, you don’t always need to visit the RBI to exchange notes, your bank is supposed to handle it.

Types of damaged notes

These are notes that are dirty, slightly torn, or worn out due to normal use.

The RBI even clarifies that a soiled note includes one that is “dirty due to wear and tear on account of normal usage” and may even include two pieces pasted together, as long as they belong to the same note and form the complete note.

These are notes that are torn or partially missing but still have identifiable features like number panels or security markings.

RBI defines it as a note “of which a portion is missing or which is composed of more than two pieces.”

These include burnt, brittle, stuck-together or badly destroyed notes that cannot be handled easily at bank counters.

RBI clearly states such notes “shall not be accepted by the bank branches for exchange” and must be taken to Issue Offices for special processing.

Where can you exchange them?

**Soiled and most mutilated notes: **Can be exchanged at any bank branch.

How much money will you actually get?

For soiled notes, there is no loss, you get full value. A torn ₹500 note still gives you ₹500.

So refusal by a bank, in most cases, is not allowed under RBI rules.

For mutilated notes, it depends on how much of the note is intact. If important details like number panels and security features are visible, RBI may still give full value. If not, you may get partial money back.

For ₹50 and above denominations, RBI follows a simple logic based on the largest intact portion:

-

If the largest piece is above 80%: full value

-

If it is 40% to 80%: half value

-

If it is below 40%: rejected

So depending on condition, you may get full, partial, or no value.

For severely damaged notes, RBI makes the final call. After inspection, you may get full value, partial value, or sometimes nothing if the note cannot be verified.

For burnt or unusable notes, there is no fixed formula. RBI evaluates them individually under a special procedure.

-

Full value

-

Partial value

-

Or no value (if authenticity/condition cannot be verified)

How many notes can you exchange at a time?

-

Up to 20 notes or ₹5,000 per day can be exchanged directly at bank counters (soiled notes).

-

For more than this, banks may accept them and credit later.

-

For mutilated notes, up to 10 pieces can be handled at branch level.

-

Larger volumes are sent to currency chest branches or RBI offices.

-

If value exceeds ₹50,000, banks are expected to take additional precautions.

"Where the number of notes presented by a person exceeds 20 pieces or ₹ 5000 in value per day, banks may accept them, against receipt, for value to be credited later. Banks may levy service charges as permitted in Master Circular on Customer Service in Banks(DBR.No.Leg.BC.21/09.07.006/2015-16 dated July 1, 2015). In case tendered value is above ₹ 50000, banks are expected to take the usual precautions, the central bank said in its banknote exchange guidelines.

If a bank does not follow proper procedure or refuses exchange unfairly, customers can approach the RBI Ombudsman under the Integrated Ombudsman Scheme. Complaints can be filed through the RBI CMS portal.

Related News

About The Author

Next Story