Market News

Week Ahead: US-Iran tensions, crude oil and gold spike, FII flows and NIFTY’s 200 EMA in focus

5 min read | Updated on March 01, 2026, 14:30 IST

SUMMARY

In the week ahead, markets are likely to remain volatile as investors monitor escalating geopolitical tensions in the Middle East, crude oil price movements, and global risk sentiment. Foreign institutional investor (FII) flows will be closely monitored, while the trajectory of crude oil prices could influence inflation expectations and the broader market.

The NIFTY50 index slipped below all the key moving averages on the daily chart, signalling weakness. | Image: Shutterstock

Indian markets ended the week on a low note, weighed down by renewed global risk-offs and sector-specific headwinds. The NIFTY50 index slipped over 1% to 25,178 for the week, ending below key moving averages amid broad-based selling across sectors. This set a negative tone for the March derivatives series.

One of the main themes was that IT stocks, as fears about AI disruption and global tech sell-offs kept the sectors under pressure. The Nifty IT index hit slipped over 4%, marking worst monthly performance in years.

At the start of the week, markets received a brief boost after a U.S. Supreme Court ruling on tariff measures sparked optimism, pushing up financial and PSU bank stocks. However, this bounce was short-lived, as broader selling re-emerged later in the week.

Towards the end of the week, geopolitical tensions escalated amid strikes involving Iran and Israel, which heightened global risk aversion. This increased selling pressure and raised concerns over global crude prices, which are a key macro trigger for Indian markets.

The impact differs across equities segments. Upstream companies such as ONGC and Oil India benefit directly from higher crude oil prices, which improves earnings visibility. Overall, as long as crude remains above key support levels, the NIFTY Energy and Oil & Gas Index is likely to remain firm. However, a breakdown in crude below its 50-day EMA could dampen sentiment across the sector.

On the domestic front, India’s growth outlook has been revised upwards under the new GDP series (with a base year of 2022–23), with real GDP in FY26 now projected at 7.6%, compared to an earlier estimate of around 7.4% using the previous methodology. Updated data also revealed that the economy expanded by 7.8% in the October–December quarter, demonstrating resilience in manufacturing and services despite global uncertainties.

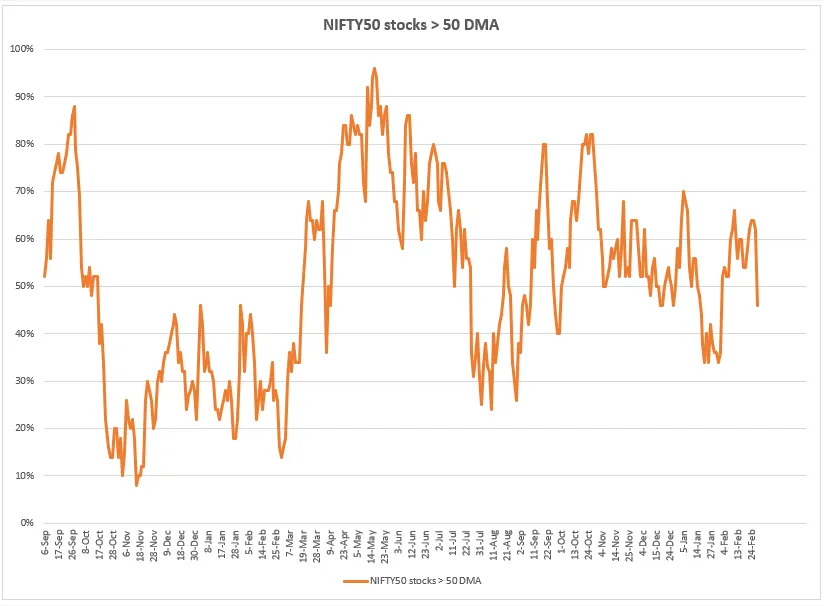

Market breadth

Market breadth remained mixed and indecisive throughout the week, with the percentage of NIFTY50 stocks trading above their 50-day moving average (DMA) fluctuating around the mid-range. However, towards the end of the week breadth of the index slips towards 35–40% zone. A sustainable bullish structure usually requires readings above 70%, whereas readings below 40% typically indicates weakness.

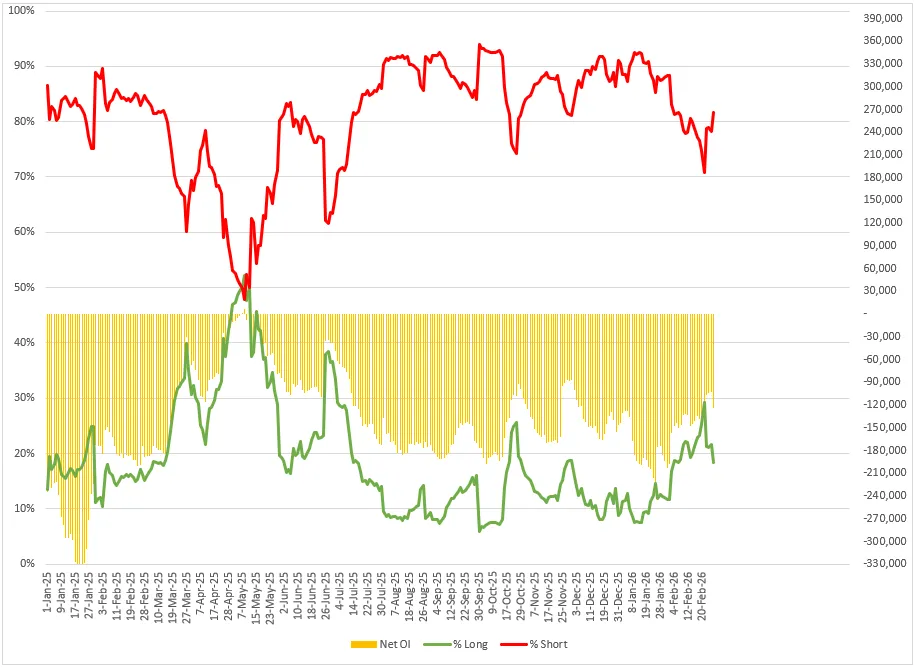

FIIs cash market and derivatives

Foreign Institutional Investors (FIIs) sustained their selling spree for the eighth month in a row and sold shares worth ₹6,640 crore in Indian equities. However, heavy selling on the last day of trading wiped out those gains, reversing the trend of the previous month and continuing the pattern of sharp fluctuations.

Meanwhile, in the derivatives segment, the FIIs have once again started the March series on a bearish note with the long-to-short ratio of 21:79 on index futures. This means, that the FIIs net open interest and index futures position remains skewed towards the short contracts, indicaitng weakness.

NIFTY50 index outlook

The NIFTY50 index slipped below all the key moving averages on the daily chart, signalling weakness. On Friday, the index slipped below the pshcyhologically support of 200-day exponential moving average (EMAs), indicating weakness. For the upcoming sessions, the 25,600 zone, which aligns with the 50-day EMA, will act as immediate resistance. Meanwhile, the next crucial supppor for the index is now 24,900. A break below this level on a closing basis will signal further weakness.

Related News

About The Author

Next Story