Market News

Week ahead: US-Iran talks, Q4 earnings, oil prices among key market triggers to watch

.png)

6 min read | Updated on April 12, 2026, 12:17 IST

SUMMARY

In the week ahead, US-Iran developments and crude oil prices will remain key sentiment drivers. Additionally, the start of the first quarter earnings in the US and inflation data will provide further clues. On the domestic front, Q4 earnings momentum and India’s CPI/WPI inflation prints will be closely tracked.

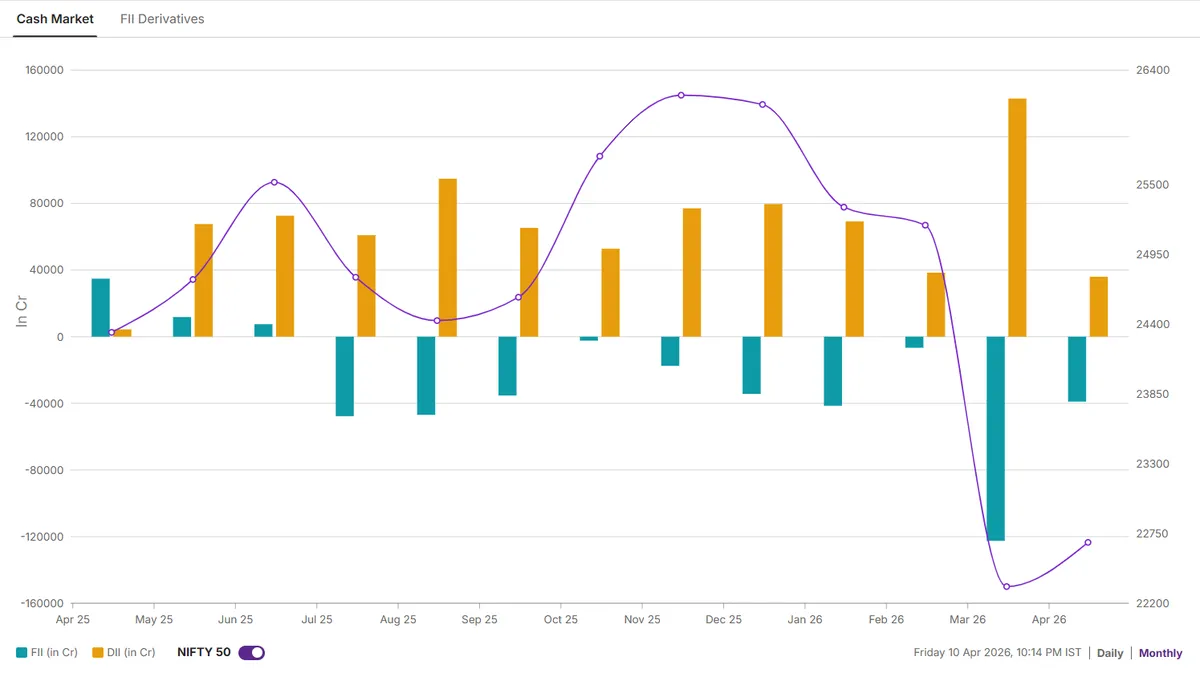

FIIs remained net sellers for the week, offloading equities worth ₹20,710 crore.

Indian markets staged a sharp rebound this week, ending their six-week losing streak. The recovery was swift and widespread, with risk appetite improving as geo-political tensions eased. The NIFTY50 index closed the week at 24,054 mark (+5.8%), and the SENSEX ended the week at 77,550 (+5.7%). The indices recovered the losses of the past three weeks and posted their best weekly performance since February 2021.

Global developments played a crucial role as signs of easing geopolitical tensions improved investor sentiment. Additionally, stability in global markets added to the positive undertone. However, the broader environment still remains sensitive to geopolitical risks and commodity price movements, which could influence sentiment going forward.

Sectorally, NIFTY Realty (+12.9%), NIFTY Auto (+10.5%) and NIFTY Consumer Durables (+9.3%) outperformed along with the Financials. On the other hand, IT( +1.9%) stocks lagged the broader market, indicating continued caution in export-oriented segments.

Overall, the market structure has improved in the near term, with NIFTY50 reclaiming the 24,000 zone. While this recovery marks a pause in the previous downtrend, the sustainability of the move will depend on follow-through buying at higher levels.

On the macro-economic data front, the U.S. Producer Price Index (PPI) will be closely watched on 14 April. Expectation remains elevated, especially driven by rising oil prices. Meanwhile, in India, inflation data will be the key trigger, with both WPI and CPI prints scheduled on 14 and 15 April. WPI inflation, after rising to 2.13% YoY in February, is expected to remain firm, supported by elevated commodity prices. On the other hand, CPI inflation, which picked up to 3.21% YoY last month, is expected to come in around the 3–3.2% range.

In India, the fourth-quarter earnings season has begun on a strong note, with IT bellwether Tata Consultancy Services beating revenue estimates. In the week ahead, key results from ICICI Prudential Asset Management Company, ICICI Lombard General Insurance, HDFC Asset Management Company, HDFC Life Insurance, and Wipro will be closely tracked.

Market breadth

The market breadth of the NIFTY50 index has shown a meaningful recovery this week, indicating improvement. The percentage of NIFTY50 stocks trading above their 50-day moving average has rebounded sharply from oversold levels. This rebound usually indicates short covering and selective buying returning across sectors after a period of weakness. However, despite this sharp recovery, the market is still not in a strong bullish zone and still below the threshold of 50%.

Foreign investors positioning

Foreign institutional investors (FIIs) remained net sellers for the week, offloading equities worth ₹20,710 crore, taking the total outflows for April to ₹38,972 crore. However, the intensity of selling has eased in recent sessions, and notably, FIIs turned net buyers on Friday. This marks their first buying day after 27 consecutive sessions of selling.

NIFTY50 outlook

NIFTY50 index staged a sharp rebound this week, rallying over 6% and gaining nearly 1,500 points from the weekly lows. On the technical front, it formed a strong bullish Marubozu candle on the weekly chart and reclaimed its 21-day exponential moving average (EMA), signalling easing selling pressure. The index also closed above the crucial 24,000 mark, indicating a shift from oversold conditions towards near-term stability.

For the upcoming sessions, the 21-EMA zone around 23,500 is expected to act as immediate support, while the 50-EMA near 24,200 will be a key resistance to watch. That said, the index continues to trade below the broader trend filter of the 200-EMA. Unless NIFTY50 decisively reclaims the 200-EMA on a closing basis, the broader structure remains weak.

Disclaimer:

Derivatives trading must be done only by traders who fully understand the risks associated with them and strictly apply risk mechanisms like stop-losses. The information is only for consumption by the client, and such material should not be redistributed. We do not recommend any particular stock, securities, or trading strategies. The securities quoted are exemplary and not recommendatory. The stock names mentioned in this article are purely to show how to do analysis. Make your own decision before investing.

About The Author

Next Story