Market News

Week ahead: RBI policy, monthly auto sales, global cues and FIIs activity among key market triggers to watch out

.png)

6 min read | Updated on November 30, 2025, 17:10 IST

SUMMARY

In the coming week, the spotlight will be on RBI policy and auto sales figures. Additionally, the markets will react to the second-quarter GDP data, which was better than expected. From a technical standpoint, the NIFTY50 index has strong support at the 25,800 level. However, the trend may remain bullish unless the index closes below this level.

Foreign institutional investors (FIIs) started the December series on a bearish note with a long-to-short ratio at 81:19, reflecting cautious approach. | Image: Shutterstock

Indian markets extended their winning streak for a third consecutive week, with benchmark indices reaching new all-time highs, despite the rupee sustaining near record low against the dollar. The NIFTY50 index rose by around 0.5% to close at approximately 26,200, reflecting consistent strength in large-cap stocks. Meanwhile, the SENSEX increased by just over half a percent over the course of the week, closing at around 85,700.

The rally occurred amid a mixed macroeconomic landscape. Optimism surrounding the potential interest rate cuts by the U.S. Federal Reserve and the Reserve Bank of India, coupled with favourable global risk sentiment, offset concerns about India–U.S. trade deal delay. Meanwhile, the weakness in Rupee against the dollar remained a cause of concern despite markets hitting fresh all-time high.

The broader markets also remained mixed with NIFTY Midcap 150 index rose 1.1% to 22,395, while the Smallcap 250 index closed flat at 16,732. In terms of sectors, leadership was fairly broad-based. The Pharma, PSU Banks and Metals posted weekly gains of between 1% and 2, while the Defence and Oil & Gas indices saw modest declines of around 1%.

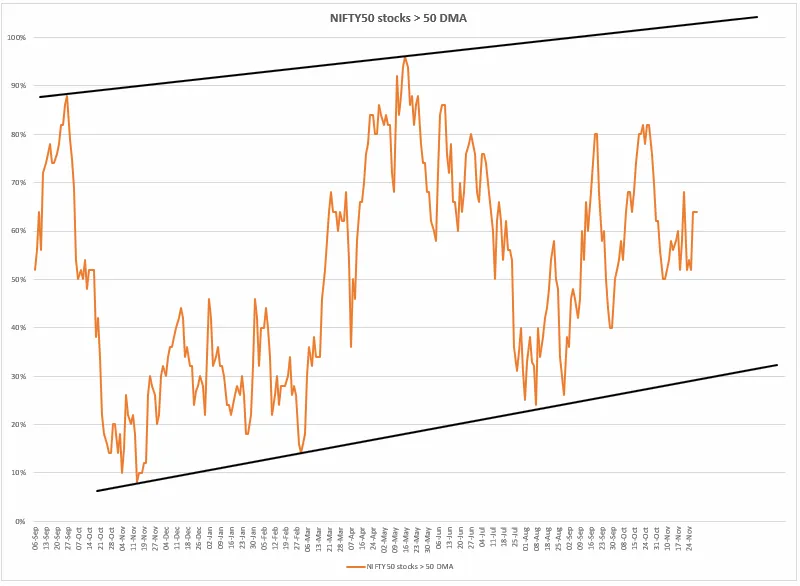

Index breadth

The breadth indicator for this week shows a stable yet tentative recovery in market participation, with roughly 60–65% of NIFTY50 constituents trading above their 50-day moving average. This level indicates that the index is comfortably in bullish territory but well short of the overextended zone. Additionally, the longer-term rising trend line of breadth (visible since late last year) remains intact. It signals that this week’s upside in NIFTY is backed by broader market participation rather than narrow leadership.

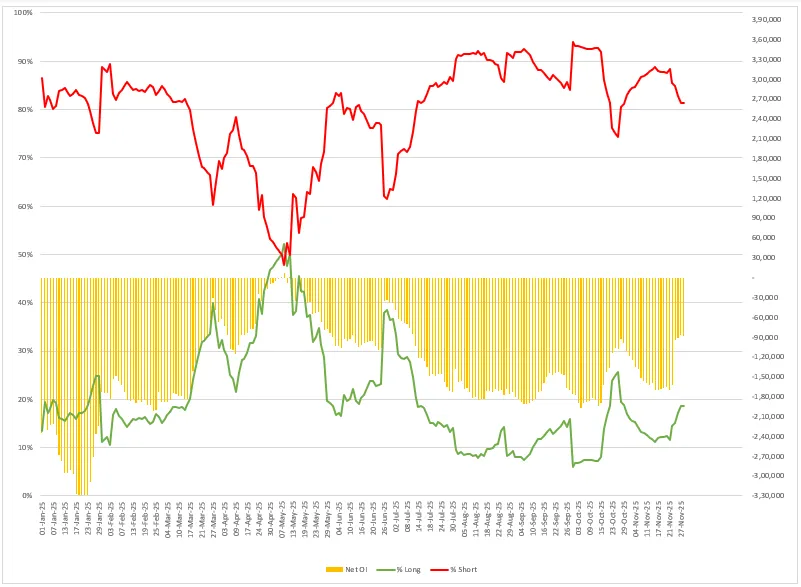

FIIs positioning equity and derivatives

Foreign institutional investors (FIIs) started the December series on a bearish note with a long-to-short ratio at 81:19 which clearly reflects a cautious approach. Although the overall open interest remains subdued compared to previous month. However, the FIIs have not yet built up aggressive directional exposure and their net open interest (OI) remains well below average peaks. This lighter OI footprint indicates that FIIs are willing to exploit the uptrend, but are doing so with limited exposure.

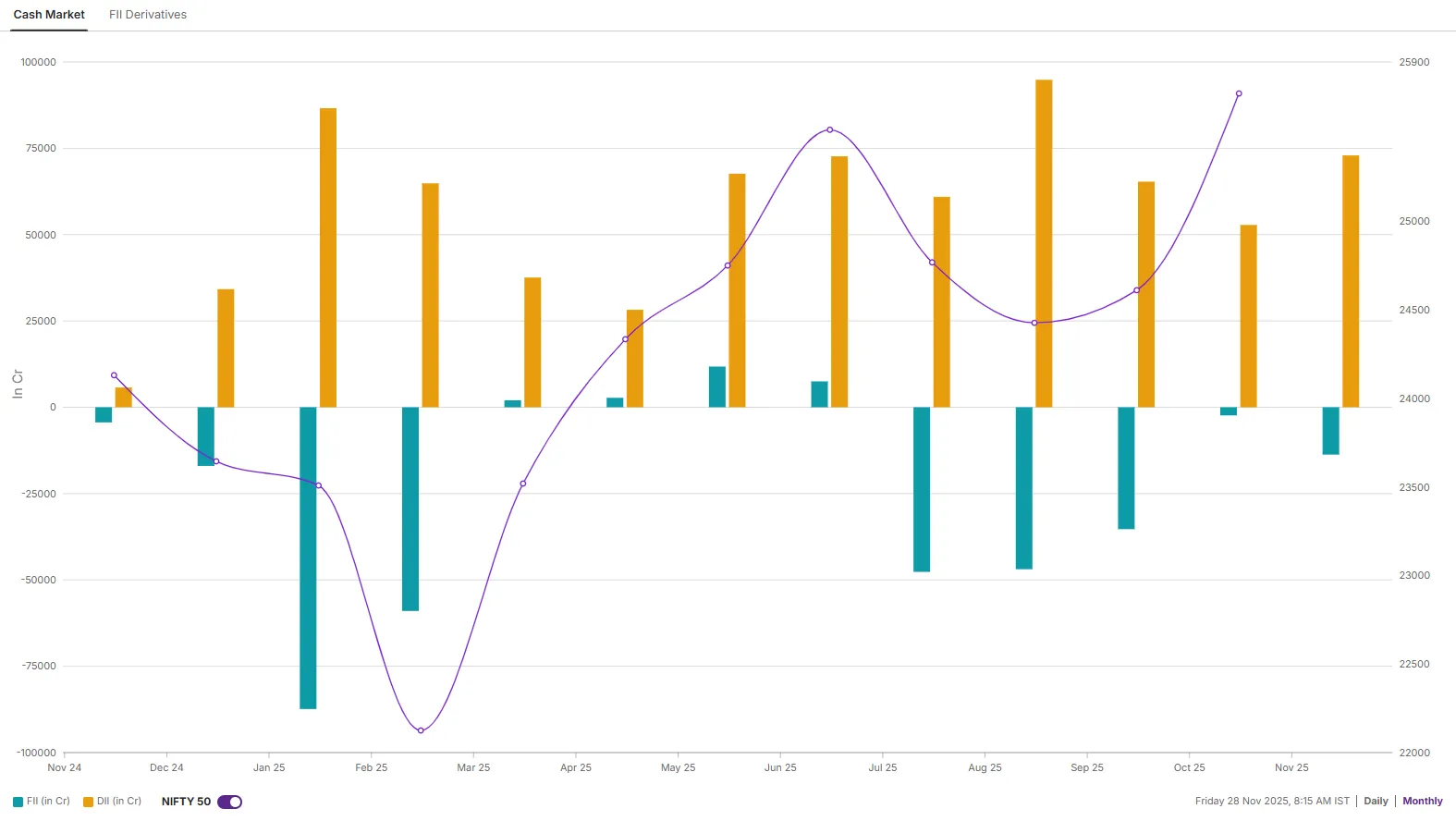

Meanwhile, in the cash market, FIIs remained net sellers in November, offloading shares worth about ₹17,500 crore. On the other hand, Domestic Institutional Investors provided strong counterbalance, deploying a substantial ₹77,038 crore and cushioning the downside pressure on equities.

NIFTY 50 index

The NIFTY50 index extended its bullish momentum, breaking out to a new all-time high for the first time in nearly 14 months. On 26 November, the index rallied by more than 1% and formed a strong bullish candle, signalling aggressive buying interest at higher levels. Notably, NIFTY continues to trade above key short-term exponential moving averages (EMAs), such as the 21-day and 50-day EMAs. This confirms the index's underlying strength and trend alignment across timeframes.

.webp)

.webp)

Additionally, the auto stocks will be also reacting to November sales data which will be released early next week. The Indian original equipment manufacturer (OEMs) expected to report their monthly wholesale dispatch numbers in the first 2–3 trading sessions, followed by retail reads from industry bodies like FADA and high-frequency VAHAN registrations with a short lag.

Ahead of the Federal Reserve's meeting in December, Chair Jerome Powell will deliver brief remarks and participate in a panel discussion at the Hoover Institution’s George P. Shultz Memorial Lecture Series on 4 December. Investors will closely analyse the event for new insights into the economic outlook and the path of monetary policy, particularly in light of the delayed release of government data due to the shutdown.

The Reserve Bank of India (RBI) will announce its monetary policy decision on December 5. Against a backdrop of benign inflation, stable liquidity and robust macroeconomic conditions, there are high expectations that the central bank will cut its repo rate by 25 basis points to 5.25%. The RBI has held rates at 5.5% since August, following cumulative cuts of 100 basis points in the first half of the year.

About The Author

Next Story