Market News

Week ahead: Q2 earnings, Fed minutes, FIIs activity and NIFTY breakout among key market triggers to watch

.png)

4 min read | Updated on July 05, 2026, 13:02 IST

SUMMARY

Indian equities enter the new week after a four-week rally, led by strong gains in realty stocks and a breakout in the NIFTY50. Track TCS results, US Fed minutes, Crude oil prices, FII flows, market breadth and key support-resistance levels for the next market direction.

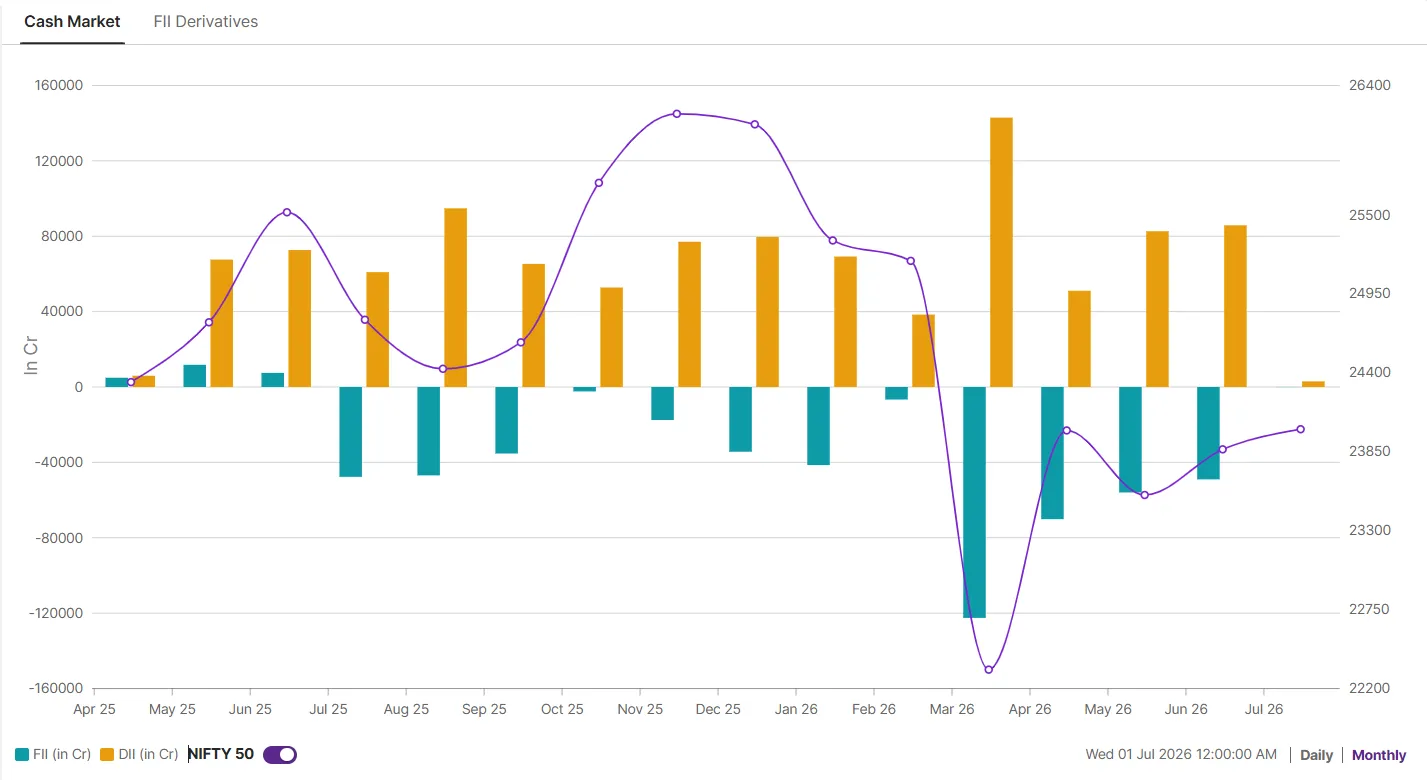

Foreign investors have started the July series on a positive note with net buying of ₹99 crore in the cash market.

NIFTY50 extended its winning streak to four weeks and closed at 24,270on July 3, up 0.9% for the week. The index moved closer to a two-month high, supported by softer crude oil prices, easing geopolitical tensions, revival in the monsoon and optimism around a possible India–U.S. trade agreement. The Sensex also gained 0.8% during the week to close at 77,763.

Sectoral participation remained broadly positive, with the Real-Estate index emerging as the top performer, rising nearly 8%, Pharma and Healthcare indices gained around 3% each, while Capital Markets and Defence indices advanced nearly 2%. On the other hand, PSU Banks fell 2.6%, while Energy and Private Bank indices closed lower for the week.

The market will enter the new week with a relatively light domestic macro calendar, while the start of the June-quarter earnings season will remain in focus.

The key question is whether the rally can sustain after such a sharp weekly move. For the coming quarter, investors will watch pre-sales guidance, new-launch pipelines, inventory trends and management commentary on affordability.

Globally, the economic calendar is also relatively light, giving traders a brief pause before the U.S. earnings season gathers pace from July 14, when major banks begin reporting. The minutes of the Federal Reserve’s June 16–17 policy meeting on Wednesday will be a crucial release. The minutes will be closely watched for clues on the Fed’s assessment of inflation, growth and the path of interest rates.

For Indian markets, lower crude remains supportive for the rupee, inflation outlook and sectors such as paints, aviation, interest rate sensitives and oil-marketing companies. However, any setback could quickly bring back a geopolitical risk premium in crude prices.

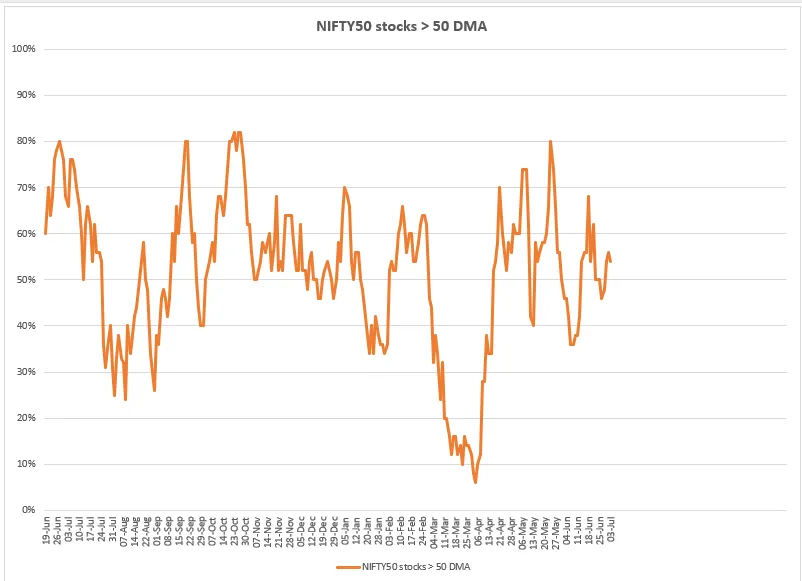

Market breadth

Market breadth improved during the week, in line with the NIFTY breakout above its recent consolidation range. The percentage of NIFTY50 stocks trading above their 50-day moving average rose to around 55 %, from nearly 46% in the previous week. This indicates that participation has improved beyond a few index heavyweights, although it is still below the 60–70% zone that would reflect a broader and more decisive market-wide uptrend.

Foreign investors positioning

Foreign investors have started the July series on a positive note. FIIs have remained net buyers in the cash market so far, with net purchases of around ₹99 crore. While the buying is modest, it marks an improvement after the sustained selling seen in the previous few months. The key question is whether FII buying improves as the NIFTY50 holds above the 24,200–24,250 breakout zone.

NIFTY50 outlook

NIFTY50 broke above its nine-session consolidation range and closed at 24,270, above the 24,200–24,250 resistance zone. The breakout has improved the short-term structure, with the index now trading above both the 20-day EMA at 23,913 and the 50-day EMA at 23,883.

The positive directional indicator has also moved above the negative indicator, indicating that buyers have regained near-term control. However, the ADX remains low at 12.3, suggesting that the new up-move has not yet developed into a strong trend.

Disclaimer:

Derivatives trading must be done only by traders who fully understand the risks associated with them and strictly apply risk mechanisms like stop-losses. We do not recommend any particular stock, securities, or trading strategies. The securities quoted are exemplary and not recommendatory. The stock names mentioned in this article are purely to show how to do analysis.

About The Author

Next Story