Market News

Week ahead: Impact of US tariff verdict, US-Iran tensions, Crude oil gain among key market triggers to watch

4 min read | Updated on February 22, 2026, 12:44 IST

SUMMARY

In the week ahead, markets are likely to remain sensitive to global developments, with Trump’s tariff stance, Nvidia’s earnings, rising US–Iran tensions and movements in crude oil prices set to dominate sentiment. Any escalation in geopolitical risks or sharp swings in oil could add to volatility, while Nvidia’s results will be closely tracked for cues on global tech demand.

NIFTY50 index has immediate support is around 25,400 to 25,350 level. | Image: Shutterstock

NIFTY and SENSEX ended the week with modest gains of 0.3%, despite ongoing volatility, weak IT stocks, and uncertainty surrounding global tariffs. The indices witnessed cautious optimism and traded in a narrow range. However, the IT sector's ongoing weakness restrained the overall upward momentum.

Market volatility also remained elevated because of global geopolitical developments, fluctuations in oil prices, and changes in U.S. trade policy. On Friday, the U.S. Supreme Court overturned President Donald Trump's trade tariffs imposed under IEEPA. However, President Donald Trump said that, after a detailed review of court’s decision, he would raise the worldwide tariff to 15% percent. This comes after he approved 10% global tariff on imports from all countries on Friday.

Sectoral performance was mixed during the week. The PSU Bank index led the gains with a climb of 5.5% followed by the Energy index with a rise of 2.4% and the FMCG index with an increase of 1.7%. Meanwhile, the Pharma and Defence indices each posted modest gains of around 1%. In contrast, the Auto and IT indices underperformed, falling between 1.3 and 2.5 % during same period.

.webp)

Meanwhile, in India, fourth quarter GDP numbers will be released on Friday. The Indian economy expanded by 8.2% in the third quarter, up from 7.8%, reflecting strong growth and momentum.

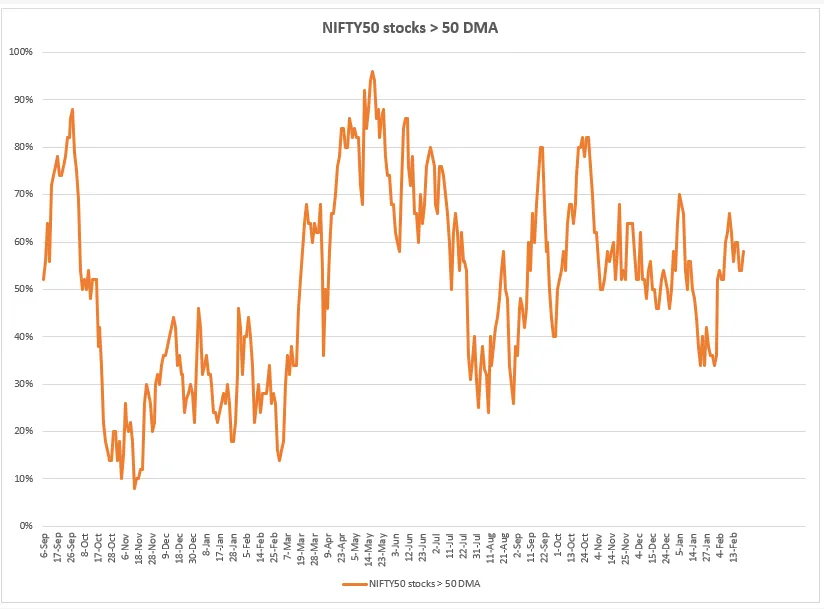

Market breadth

NIFTY’s market breadth moderated this week mildly, with the percentage of NIFTY50 stocks trading above their 50-day moving average from 60% to 58%. The decline is marginal and suggests mild cooling rather than a structural deterioration in participation. While the broader tone remains stable, sustaining breadth above the 60% zone would be important to support further upside momentum.

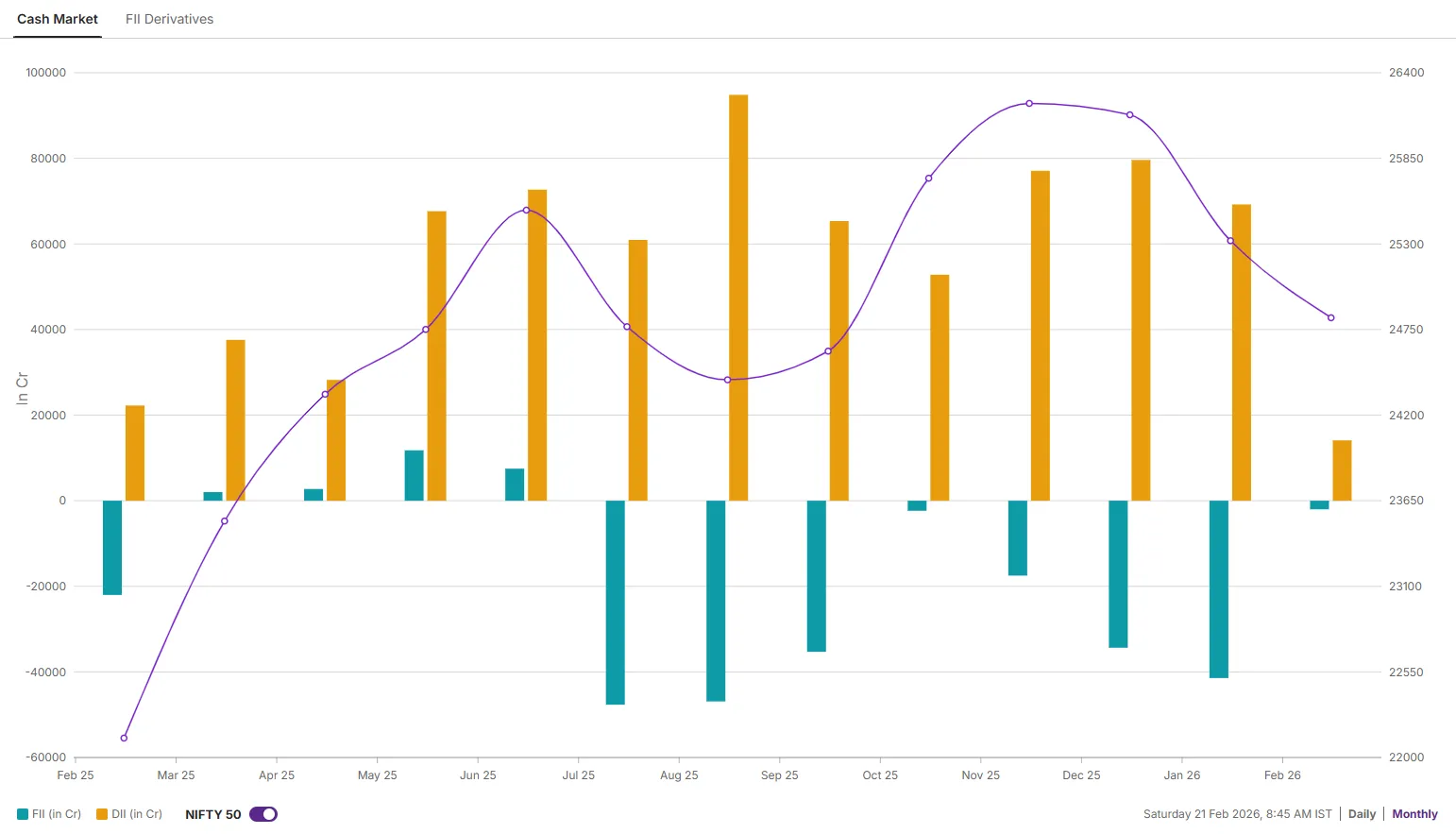

FIIs cash market and derivatives

Foreign Institutional Investors (FIIs) activity in the cash market remain muted in the month of February and have sold shares worth ₹2,011 crore. Meanwhile, Domestic Institutional Investors (DIIs) supported the markets and have purchased shares worth ₹14,111 crore.

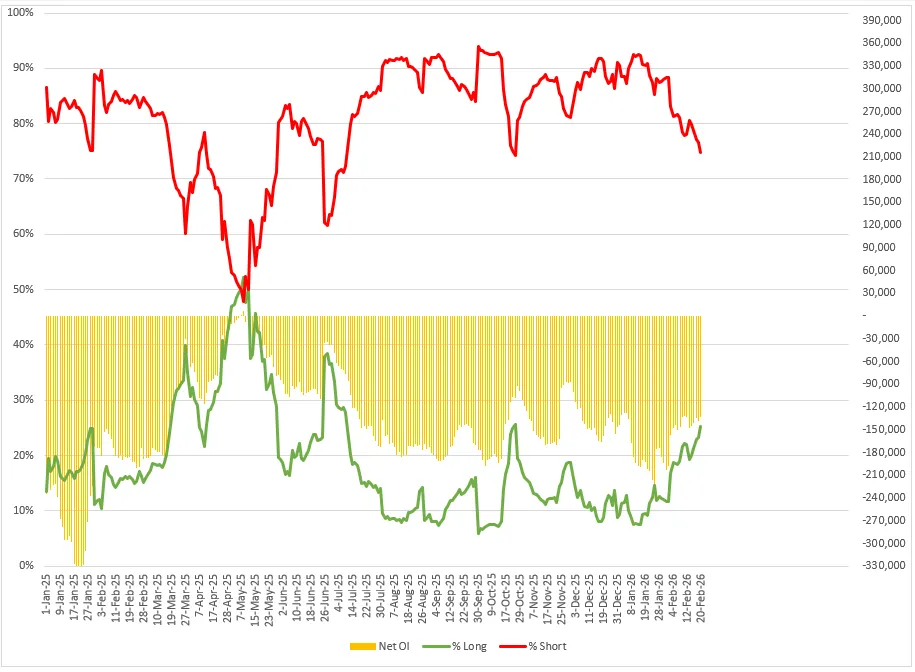

In the derivatives segment, the long-to-short ratio of FIIs in index futures cooled from 20:80 to 25:75 as the FIIs gradually reduced the short contracts in index futures. Additionally the net open interest of the FIIs in index futures dropped 8% to 1.33 lakh contracts (-ve), indicating covering of some short contracts.

NIFTY50 outlook

NIFTY50 index protected the immediate support zone of 25,400 and 25,350 on the closing basis and failed to confirm the bearish engulfing candle on the daily chart, formed on 19 February. After rebounding towards the 21-day and 50-day exponential moving averages (EMAs), the index faced resistance around these levels and failed to capture on these zones on a closing basis. In the short-term, the index is trading between the immediate swing high (25,885), which will act as a resistance. On the flip side, the immediate support is around the 25,400 and 25,350 zone. A break of this range on a closing basis will provide further clues.

.webp)

Disclaimer:

Derivatives trading must be done only by traders who fully understand the risks associated with them and strictly apply risk mechanisms like stop-losses. The information is only for consumption by the client, and such material should not be redistributed. We do not recommend any particular stock, securities, or trading strategies. The securities quoted are exemplary and not recommendatory. The stock names mentioned in this article are purely to show how to do analysis. Make your own decision before investing.

About The Author

Next Story