Market News

Expiry trade setup for March 30: Can NIFTY50 defend 22,400 on Monday?

.png)

5 min read | Updated on March 30, 2026, 08:42 IST

SUMMARY

GIFT NIFTY futures indicate a sharp gap-down opening for Indian markets on Monday. The global market cues remain weak as escalating tensions in the Middle East have unnerved investors' sentiment.

NIFTY50 is expected to open nearly 300 points lower on Monday morning, owing to weak global market cues. Image: Shutterstock.

GIFT NIFTY futures traded nearly 300 points lower on Monday morning, following the global market cues, indicating a weak opening for Indian markets on Monday. The Asian markets plunged as much as 4.5% on Monday morning as tensions escalate in the Middle East region.

Crude oil prices surged above $105 per barrel on Friday after the US and Iran talks failed to yield a positive outcome. Mixed reactions and comments from both parties on the ongoing conflict have left investors nervous about the geopolitical outlook. The crude oil prices extended the gains on Monday morning by rising another 2%.

US markets closed deep in the red, with all the major benchmark indices falling as much as 1.9% on Friday. US markets are on the verge of the worst monthly sell-off since September 2022, having lost 7.7% in March so far.

On the domestic front, the Indian rupee will remain in focus after the RBI asked Indian banks to unwind their long dollar positions. Under the new rule, banks need to limit their net open position in the Indian rupee (NOP-INR) to $100 million by April 10. The move is expected to bring a sharp appreciation in the local currency as banks will have to sell dollars and buy rupees to comply with the new rule.

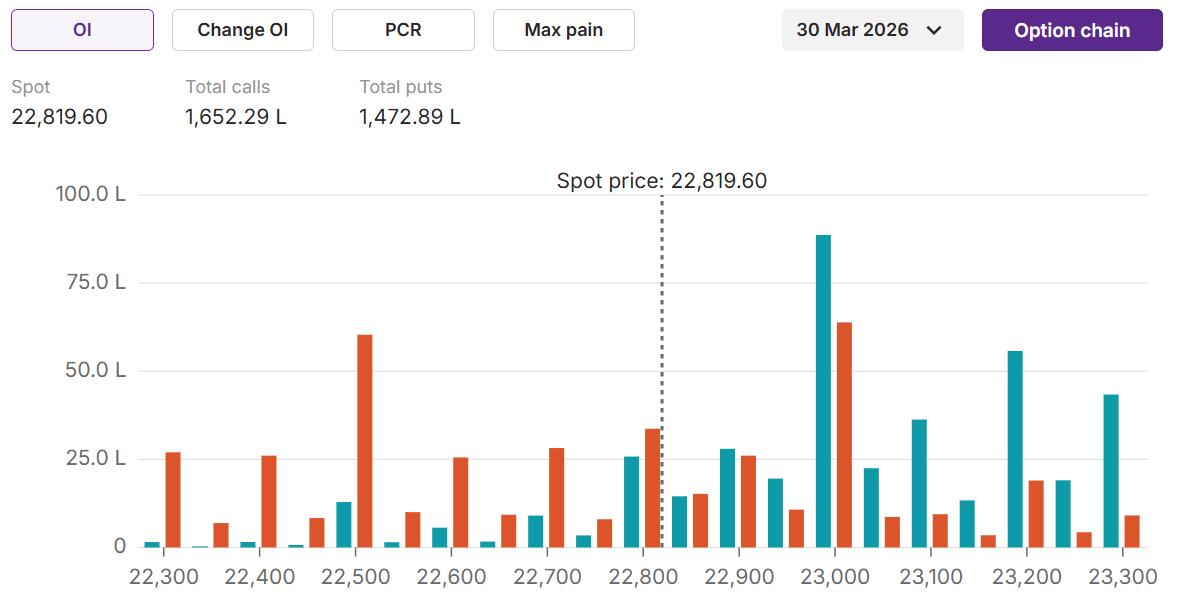

- Implied trading range: 22,400 to 23,400

- OI resistance: 23,000

- OI support: 22,000

- Structure: Rangebound

- Intraday tone: Bearish below 22,400

Open interest data

Positioning

| Trend | Friday | Wednesday |

|---|---|---|

| FIIs index short% (Futures) | 85% | 85% |

| PCR | 0.89 🔽 | 1.25 |

| OI (23,000 CE strike) | 88 lakh 🔼 | 30 lakh |

💰 Institutional intelligence

Foreign institutional investors (FIIs) have consistently remained sellers throughout March, offloading equities in all 18 trading sessions so far. Total sales stood at ₹1,11,377 crore, making it the second-highest monthly outflow since October 2024.

This sustained selling has been reflected in their derivatives positioning as well. FIIs began the March series with a long-to-short ratio of 21:79 in index futures, indicating a clear bearish bias with nearly 79% of positions on the short side.

That trend has only intensified. The long-to-short ratio stayed heavily skewed towards shorts throughout the series and stood at 15:85 as of March 27, with net open interest at -2.79 lakh contracts. Even on monthly expiry and ahead of April rollovers, FII positioning continues to signal a firmly bearish stance.

- Resistance: 23,450

- Support: 22,450

- Call concentration: 23,000

- Put concentration: 22,000

- Bullish above: 23,450

- Bearish below: 22,450

-

Price: Below 20 EMA and 50 EMA

-

RSI: 40 (Neutral)

-

ADX: 19 ( non trending)

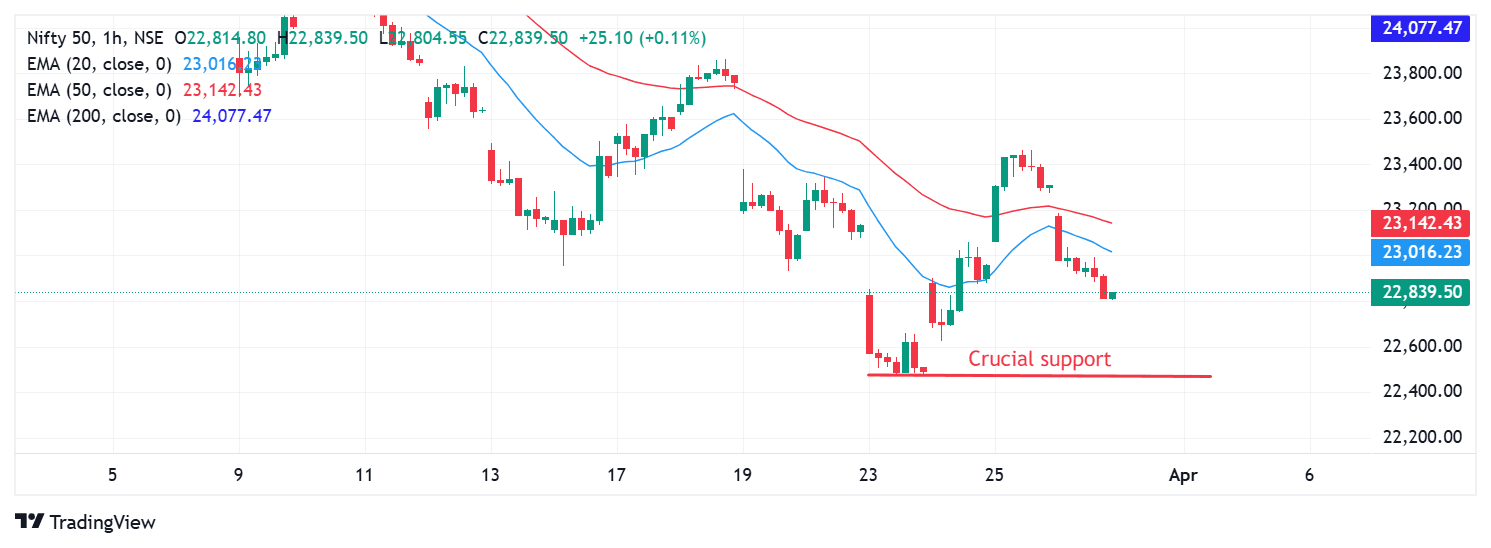

The NIFTY50 index gave up all the major gains of previous two trading sessions on Friday by closing below 23,000. Scepticism grew around negotiation talks between the US and Iran amid the ongoing conflict.

On the hourly charts, the index closed below the 20 and 50 EMA levels, reversing the bullish sentiment in the markets. On the long-term charts, the recent 52-week low of 22,471 remains the next crucial support level. A closing below that may trigger further selling towards 22,000 and the upside remains capped at 23,000 levels.

If–then playbook

A daily close above the 23,450 zone would be the first sign of the index shifting towards a higher high, higher low structure. Until this level is reclaimed on a closing basis, the trend is likely to remain sell-on-rise.

A close below this zone, which aligns with the immediate swing low of March 23, would signal emerging weakness. In that case, the next key support levels come in at 21,900 and 21,700. This implies a potential downside of up to 5% from the March 27 closing level. If the index drifts into this zone, the drawdown from the all-time high (January 5) would widen to over 17%. At that stage, traders should avoid initiating fresh short positions, as the risk-reward equation becomes unfavourable.

About The Author

Next Story