Market News

HDFC Bank Q4: Net profit could see single-digit rise; focus on management commentary and dividend

4 min read | Updated on April 17, 2026, 12:20 IST

SUMMARY

HDFC Bank is expected to report modest Q4 growth, with profit rising around 7 to 8% YoY and NII up 4 to 6%. Investors will focus on margins, asset quality, management commentary, and the final dividend.

Stock list

As of 17 April, the options market is pricing in a move of about ±4.9% in HDFC Bank shares.

India's largest private sector lender, HDFC Bank, will announce its March quarter results on April 18, 2025. Ahead of the results, the bank released its business update for the fourth quarter of FY26.

Q4FY26 business updates

HDFC Bank reported a 12% YoY increase in gross advances to ₹29.60 lakh crore during the fourth quarter. The bank’s deposits grew by 14.4% YoY, totalling ₹31.05 lakh crore. Its current account-savings account (CASA) deposits also rose by 12.3% YoY, reaching ₹10.6 lakh crore during the quarter.

As per experts, HDFC Bank could report single-digit growth in net profit and net interest income (NII) with key focus on management commentary, business outlook and final dividend announcement.

HDFC Bank is expected to report 7.5% to 8.4% YoY growth in net profit to ₹18,950 to ₹19,110 crore. Sequentially, net profit could see modest growth of 1% to 2%. The private lender registered a standalone net profit of ₹17,616 crore in Q4FY25 and ₹18,654 crore in the previous quarter.

Net interest income (NII) is likely to increase by 4% to 5.7% YoY in the range of ₹33,600 to ₹33,720 crore, while remaining flat compared to the previous quarter. HDFC Bank reported an NII of ₹32,615 crore in the previous quarter, while it stood at ₹32,070 crore in Q4FY25.

HDFC Bank investors will look forward to management commentary on credit and deposit growth, margin outlook and track key performance indicators like net interest margin, gross and net non-performing assets (NPAs). Investors will also watch out for the impact of rising bond yields and the imposition of a $100-million cap by the RBI on open rupee position in the foreign exchange market on treasury income.

Ahead of the Q4 result announcement, HDFC Bank shares are trading 0.5% higher at ₹799 apiece on NSE. So far this year, HDFC Bank shares are down nearly 20%.

Technical outlook

HDFC Bank remains in a broader downtrend, trading below its 20, 50 and 200 EMAs, although a short-term pullback has emerged from the ₹725 lows. The stock is currently facing resistance near the ₹810–₹820 zone, and unless it decisively closes above this level, the recovery may remain capped.

A breakout above ₹820 can push the stock towards the ₹840–₹850 zone (50 EMA), while on the downside, failure to hold ₹780–₹790 could drag it back towards the ₹725 support, with a break below this level likely to resume the primary bearish trend.

Options outlook

As of 17 April, the options market is pricing in a move of about ±4.9% in HDFC Bank shares, based on the at-the-money 795 strike and current implied volatility.

That expectation rises slightly to around ±4.9%, which opens the door for strategies like long or short straddles, depending on how a trader views potential price movement and volatility.

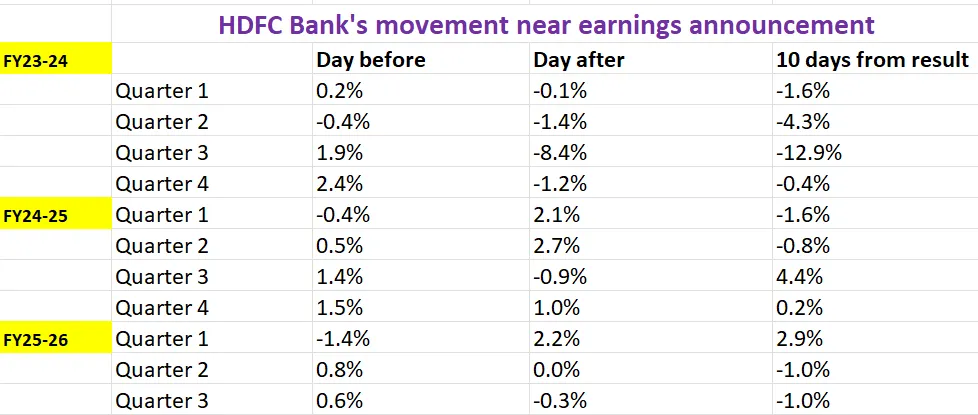

Before getting into those strategies, it helps to look at how the stock has reacted to earnings over the past 11 quarters.

Options strategy for HDFC Bank

With the options market pricing in a ±4.9% move for HDFC Bank ahead of the 28 April expiry, traders may look at straddle strategies.

A long straddle means buying both an at-the-money call and put with the same strike and expiry. This setup works if the stock moves more than ±4.9% in either direction.

A short straddle takes the opposite view. It involves selling both the ATM call and put, aiming to benefit if the stock stays within that ±4.9% range and volatility eases.

Disclaimer:

Derivatives trading must be done only by traders who fully understand the risks associated with them and strictly apply risk mechanisms like stop losses. The information is only for educational purposes. We do not recommend any particular stock, securities or strategies for trading. The stock names mentioned in this article are purely for showing how to do analysis. Take your own decision before investing.

About The Author

Next Story